Choosing an Index for Your Climate Transition Strategy

It might sound counterintuitive, but our research shows a standard market index is often a better benchmark for climate-transition strategies than a climate-focused index.

Key takeaways

- Standard market indexes provide greater flexibility without restricting sustainability and investment performance.

- Climate-focused indexes that use exclusions are backward-looking. For example, reported carbon intensity doesn’t capture a company’s commitments to future decarbonization.

- Standard market indexes start with a broader opportunity set. Climate and financial goals can be achieved by applying forward-looking analysis to identify leading firms.

One of the most important questions to address when investing in a climate transition strategy is, “Which index should we use as a benchmark?” This choice affects a range of outcomes, from security selection and performance to reporting and stakeholder communications.

To help investors answer this question for their own fixed income portfolios, we review:

- Indexes commonly used for fixed income climate strategies

- A comparison of standard market indexes and specialized climate indexes

- Trade-offs investors should understand before making a decision

Three types of indexes

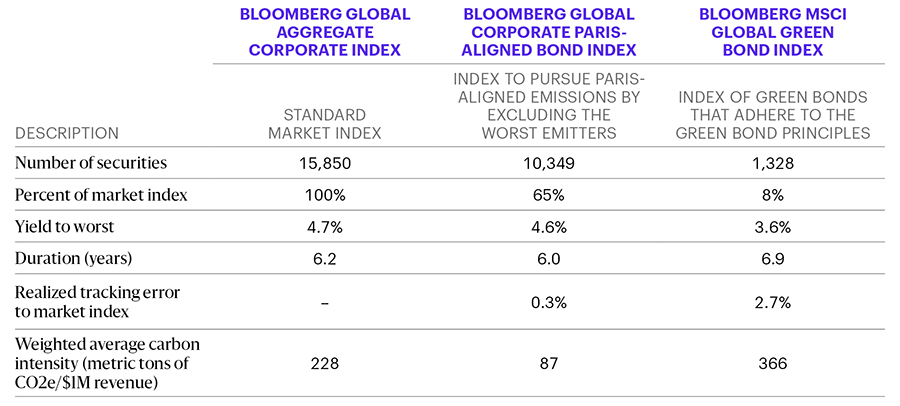

When managing fixed income strategies with climate transition objectives, investors can choose a standard broad market index for their benchmark (such as the Bloomberg Global Aggregate Corporate Index) or a more specialized, climate-focused index (such as the Bloomberg Global Corporate Paris-Aligned Bond Index or Bloomberg MSCI Global Green Bond Index). Even if an investor has ambitions related to the European Union’s Paris-aligned goals, they may have the option of using a standard benchmark, which could also better suit their overall needs.

Figure 1 shows three types of indexes used to benchmark climate fixed income strategies, based on a review of the Morningstar Global Corporate Bond UCITS universe. Roughly three-fourths of climate strategies are managed against a standard market index, while the rest typically use a Paris-aligned or green bond index. We limit our review to these three index types, recognizing there’s a growing range of climate indexes available in fixed income.

FIGURE 1: COMPARING POPULAR INDEXES FOR CLIMATE FIXED INCOME STRATEGIES

Sources: Allspring, Trucost, and Bloomberg Finance LP, as of December 31, 2023. The Bloomberg Global Aggregate Corporate Total Return Index Hedged USD represents the standard market index. The Bloomberg Global Corporate Paris-Aligned Bond Index Unhedged USD represents the Paris-aligned index. The Bloomberg MSCI Global Green Bond Index Total Return Index Value Unhedged represents the green bond index. Tracking error is ex post and annualized for 35 monthly returns.

The Paris-aligned index in this example covers 65% of the standard market index with limited differences in other characteristics (such as yield and duration) while achieving a much lower carbon intensity.

Green bonds are a well-established category, and bond proceeds can have a number of specific uses (such as renewable energy, pollution prevention, clean water, green buildings, and climate adaptation). From an investment perspective, green bonds are only a small subset of the market index (8%), with quite different investment metrics. It may surprise investors that the carbon intensity of the green bond index is higher than that of the market index. This reflects the fact that high-emitting firms tend to dominate green bond issuance (for example, utilities and energy producers). We believe green bond indexes’ narrow focus makes them impractical benchmarks for most climate transition strategies, so from here we focus on the Paris-aligned and standard market indexes.

Specialized indexes present trade-offs for investors

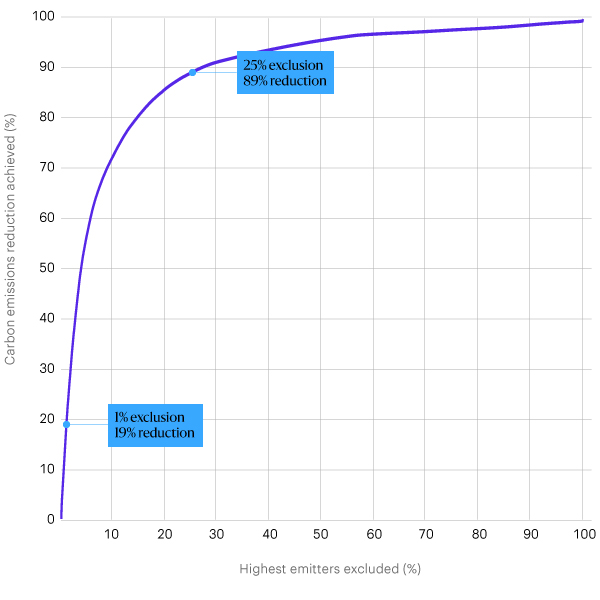

Paris-aligned and other specialized, climate-focused indexes tend to exclude high-emitting firms and industries, which can help build portfolios with low carbon intensity. Figure 2 shows how a small number of very high emitters dramatically elevates the standard index’s emissions intensity. Excluding these heavy emitters results in large intensity reductions. For example, excluding only the top 1% of emitters results in a whopping 19% reduction in carbon intensity; excluding the top quartile of emitters achieves an 89% reduction in carbon intensity.

FIGURE 2: FEW EXCLUSIONS ARE REQUIRED FOR LARGE REDUCTIONS IN CARBON INTENSITY

Sources: Allspring, Trucost, and Bloomberg. Data as of December 31, 2023.

However, it’s far from clear that these exclusions help investors achieve their climate transition and financial goals. Reported carbon intensity is a backward-looking metric—it doesn’t capture an issuer’s forward-looking climate profile. In fact, we expect to see the largest contributions to decarbonization from today’s high emitters that have detailed strategies and budgets committed to future decarbonization.

This has been the case when we’ve looked at the largest contributors to decarbonization within the standard market index. The companies that achieved the largest decrease in emissions have typically been companies with high emissions. Focusing solely on today’s lowest emitters could mean missing out on greater decarbonization—and investment—opportunities.

Beyond the investment and decarbonization opportunities, investors should understand additional trade-offs when considering specialized climate-focused indexes:

Event risk: Currently, most banks report mainly on direct emissions—that is, emissions generated by a bank’s operations as opposed to those of a bank’s customers and suppliers. That has begun to change. Especially in Europe, regulations increasingly require banks to also disclose emissions associated with lending and underwriting activity, likely revealing that banks are more emissions-intensive than historical reports suggest. If this continues, climate index providers may need to rebalance indexes quickly, reweighting (and possibly even removing) some constituents to preserve their indexes’ green credentials. Given the high weighting of banks in a typical Paris-aligned index (shown in Figure 3), this presents significant event risk to investors using these indexes as climate-transition benchmarks.

FIGURE 3: BANKS ARE A MAJOR COMPONENT OF STANDARD MARKET AND PARIS-ALIGNED INDEXES

Sources: Allspring, Trucost, and Bloomberg Finance LP. Data as of December 31, 2023.

Engagement opportunities. Engaging with issuers on climate and other sustainability-related issues can be a powerful tactic for investors seeking to encourage disclosure and/or change corporate behavior. Index choice doesn’t necessarily restrict the range of firms with which an investor will engage, but standard indexes naturally expose and encourage investors to engage with a more diverse array of firms. This inclusive approach expands opportunities for investors to support positive environmental and social change.

Opportunity set. A climate-focused investment strategy should help investors prioritize firms best positioned to achieve climate and financial objectives. This is a complex undertaking. Specialized indexes mainly attempt this by reducing the investment opportunity set, based on industry and firm activities and historical emissions. Rather than shrinking the opportunity set, we believe climate and financial objectives are best achieved with thorough, thoughtful, and forward-looking analysis of issuer activity, operating expertise, and climate risk management. For example, Figure 3 illustrates the lost opportunity to invest in energy and utility firms that may be tomorrow’s decarbonization leaders. Many of these firms may be high emitters today, but these sectors are key to achieving a net-zero economy. Choosing an index is the first step in identifying the best portfolio constituents—it doesn’t have to be the only step.

Balancing risk and return. Even with a specialized index that has a smaller universe of investable securities, investors can often select out-of-index bonds up to certain policy limits. But that’s likely to increase tracking error. A standard market index, on the other hand, can allow investors to harness the best opportunities while managing tracking error more efficiently.

Fit for purpose. While the number of specialized climate indexes is growing, that doesn’t mean these indexes are becoming more effective at achieving investors’ objectives. This is particularly true for investors seeking to support the transition across sectors of the economy to low (or no) emissions. By focusing on firms that have achieved low emissions, specialized indexes may miss opportunities to drive alpha by investing in firms that most need transition capital—those with relatively high emissions. We’re optimistic that data and processes will continue to improve, but we believe standard market indexes are presently better suited to transition-focused investment strategies.

Making the case for market indexes

Even though most climate-aware credit strategies currently use a standard market index as a benchmark, specialized, climate-focused indexes continue to grow. While our analysis shows that standard market indexes can indeed offer advantages over specialized indexes for managing climate transition portfolios, we will continue to evaluate new indexes as the sustainable investing landscape evolves.

Source: MSCI. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, reviewed, or produced by MSCI.

EU ESG

Articles 6 and 8 refer to classifications of each investment strategy that apply to products under the European Union’s sustainable finance disclosure regulation. This set of rules reveals the differing levels of sustainability integration and focus of each investment strategy that they offer.