Election 2024: The “Big Picture” for Equities

Investors face uncertainty around U.S. presidential elections, driving market volatility. How might companies be affected? Have elections affected equity returns long term? Allspring’s Ann Miletti provides perspective.

Key takeaways

- As a U.S. presidential election approaches, equity investors tend to worry about the outcome’s potential impact on their investments, driving volatility in the market.

- Ann discusses the two parties’ differing policy views in two areas plus four of each party’s priorities and types of companies that may benefit if the party prevails.

- Has the U.S. equity market been affected over the long term by previous elections? We reviewed historical returns over earlier presidential cycles to find out.

Every four years, investors deal with preelection pressure that tends to intensify in the months leading up to a U.S. presidential election. The concern stems from more than just which candidate will win—there are other big questions to worry about, too: How will the market react before and after the outcome? How might policies change, and what types of companies could be affected? Uncertainties like these fuel anxiety and fear, driving volatility in the equity market.

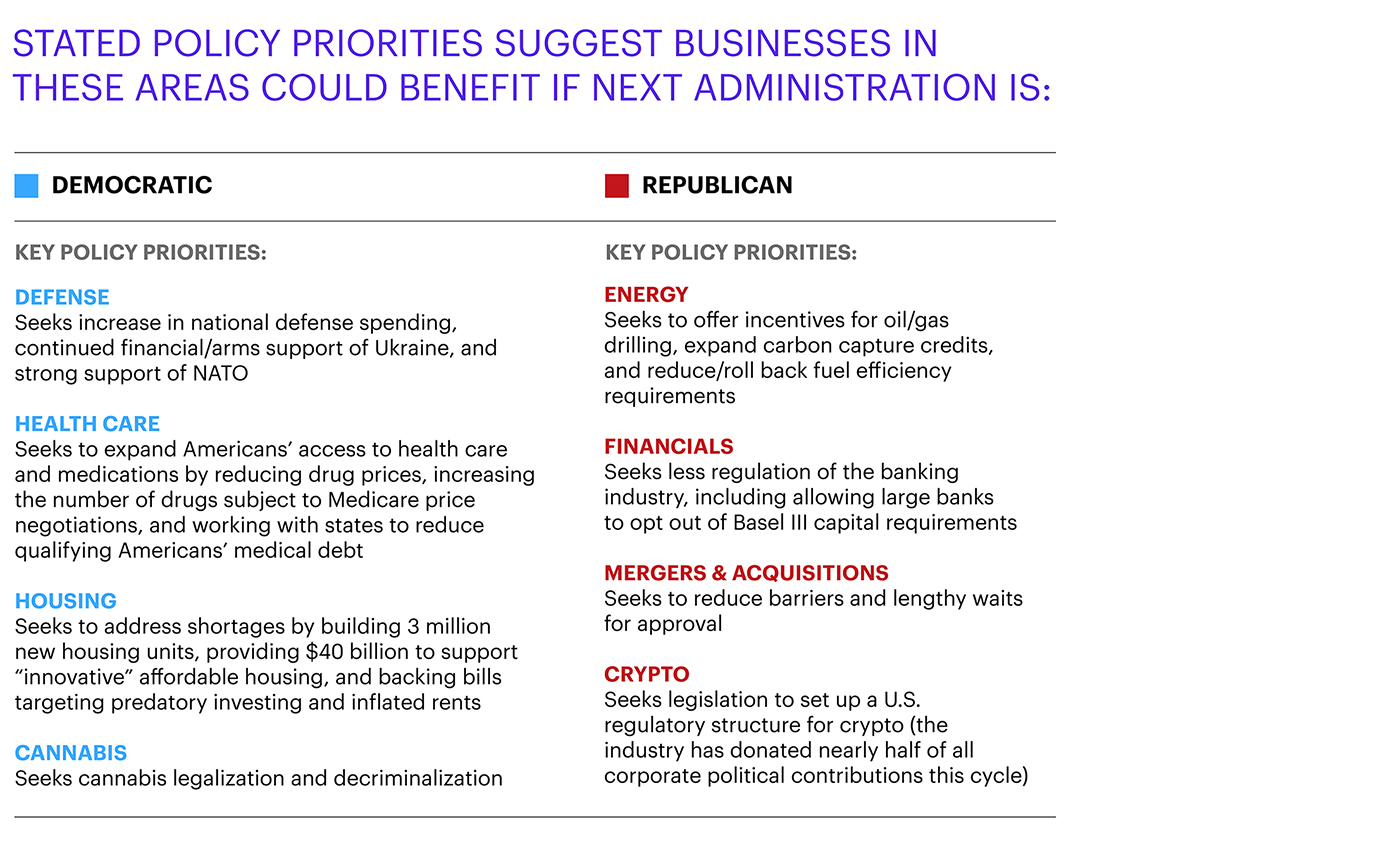

As with every presidential election, the Democratic and Republican parties’ views differ in a number of policy areas. We take a look at two key categories and at several of each party’s priorities that certain types of companies may benefit from if the party prevails.

Also, we reviewed historical total returns during earlier election cycles with this question in mind: Have previous elections actually affected the U.S. equity market over the long term? (Spoiler alert: not much. The past does not reliably predict the future, however, so it’s important to focus on managing risk, especially when volatility is high.)

Each party’s desired tax and regulatory policy changes lean toward an overarching theme.

Overall, the Republican party’s proposals emphasize lower taxes and streamlined regulations. The party’s stated objectives include cutting the corporate tax rate and the corporate alternative minimum tax. The party also seeks to reduce regulations substantially across the board.

The Democratic party’s proposals, overall, emphasize reducing inequality, supporting working families, and advancing sustainability. The party’s stated objectives include raising the corporate tax rate, adding tax credits to promote clean energy, and providing tax incentives to construct affordable housing. Regarding regulations, the party seeks changes such as raising the federal minimum wage and expanding student debt relief as well as antitrust enforcement.

There’s clear support from both parties on one important initiative: onshoring.

Bringing manufacturing and production activities back to the U.S. from overseas locations is a focus for both parties for a number of reasons, including:

- Supply chain consistency—addressing glaring risks, revealed during COVID-19 pandemic, of global supply chains of essential materials

- Geopolitical risks—reducing dependence on locations outside the U.S.

- Product integrity and protection—maintaining oversight/control of production processes and protect intellectual property/innovation

Party priorities may prove beneficial for companies in certain areas.

Priorities each party has presented may lead to potential investment opportunities if the party prevails, including those identified in the table below.

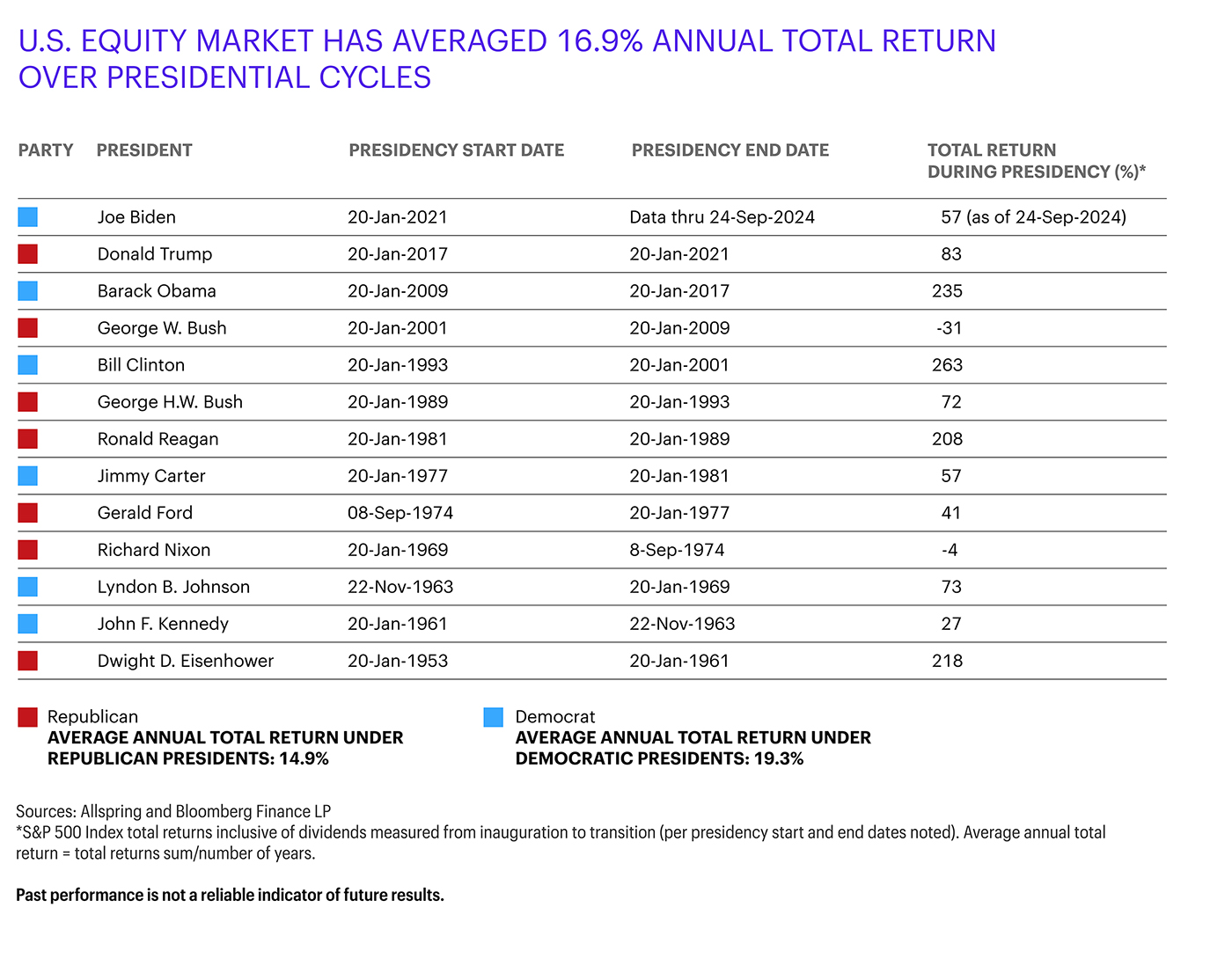

Throughout election cycles, the U.S. equity market has kept on delivering.

We calculated U.S. equity total returns during presidential cycles, starting with Dwight D. Eisenhower’s election in 1953. This table shows the results: Over time, the U.S. equity market has delivered primarily positive results over presidential cycles, through both Democratic and Republican administrations.

Expect some volatility with presidential elections—it’s OK.

As we mentioned earlier, volatility picks up around presidential elections—and when political rhetoric heats up, investors can become even more nervous. However, once the election is over and a winner is named, the U.S. equity market historically has readjusted, smoothed out, and moved resiliently forward—no matter which party was successful.

This pattern is similar to what we’ve seen transpire in the equity market in the aftermath of unexpected, extreme events that were nonpolitical—for example, the COVID-19 pandemic and the Global Financial Crisis. Following each of these shocks, the U.S. equity market recovered and subsequently delivered positive results. Companies have repeatedly demonstrated that they will adjust.

Position for pursuing financial goals and controlling risk: an all-weather equities approach

Diversification is critically important.

The term diversification is most often used in the context of spreading investments across a variety of asset classes with the goal of reducing overall portfolio risk. We believe it’s just as crucial to diversify within an asset class—especially within equities as they often represent a significant segment of investors’ portfolios.

An equities portfolio can be diversified across a variety of categories—including market capitalizations, geographic regions, sectors, industries, and styles. Beyond its primary goal of minimizing losses, diversification can also uncover potential opportunities in categories that might not have been included in a less diverse portfolio.

Focus on quality.

We believe quality is key to uncovering companies capable of success in any environment. Below are essential characteristics we look for to identify quality companies:

- Fluid cash flow: Sustainable cash generation through all parts of the economic cycle

- Well-structured balance sheet: Modest financial leverage, elongated maturity profile, margin of safety versus debt covenants

- Competitive advantage: A differentiated product or service with strong customer demand

- Proven management team: Skilled capital allocators who have experience navigating through an economic cycle

Businesses with the four qualities listed above are well positioned to succeed at clearly differentiating themselves via competitive, sustainable results in the marketplace. Note that when pursuing quality, it’s also critical to evaluate whether a specific company is an appropriate holding for the portfolio. This is especially important during times when the equity market tends to be more volatile—such as around presidential elections.

Diversification does not ensure or guarantee better performance and cannot eliminate the risk of investment losses.

Related insights

According to Derrick Irwin, senior portfolio manager and co-head of Allspring’s Intrinsic Emerging Markets Equity team, there’s potential for a sea of change in how investors allocate to emerging market equities.

Bryant VanCronkhite and John Ognar recap Q3 market trends—the shift from a "grab-it-all" low-quality rally to a focus on high-quality investments, the expanding opportunities in AI, and what to expect in Q4.

Alison Shimada and Derrick Irwin discuss why now presents a pivotal time for investors looking at the asset class. Discover the shifting global dynamics and themes shaping the future of emerging markets (EMs) from two different perspectives.

The global landscape is shifting, and structural tailwinds are lifting emerging market (EM) equities. Investors capitalizing on these trends could benefit from transformative growth opportunities for years to come.

Video

The Dividend DivideAllspring experts explore the evolving role of dividends, debating their value as a source of stability, a tool for discipline, and their impact on flexibility in today's market.

Hyperscalers are investing in artificial intelligence (AI) and infrastructure to drive innovation while navigating challenges—balancing short-term demands with long-term growth opportunities.

Insight

PM Spotlight: Wired for GrowthMike Smith is a senior portfolio manager and head of Allspring’s Growth Equity team. His team’s diversified approach focuses on stocks with robust, sustainable, and underappreciated growth across the market-cap spectrum.

Bryant VanCronkhite is a senior portfolio manager and co-head of Allspring’s Special Global Equity team. The team looks for market inefficiencies using a CPA’s knowledge and approach to analyzing financial statements.

Read the latest update from the Rising Dividend Equity team to discover what sets dividend growers apart and how they may offer a compelling allocation opportunity for investors.

Allspring equity portfolio managers Bryant VanCronkhite, Alison Shimada, and Mike Smith sit down to explore current market conditions, economic uncertainties, and potential investment strategies for 2025. They break down the unique challenges and opportunities in current equity markets and the importance of active management and resilience during times of volatility.

We discuss two risks investors face: 1) the increased risk in strategies mirroring the S&P 500 as just a few holdings drive its results, and 2) the huge wall of corporate debt maturing in 2025–2029 that will need renewal at much higher rates.

The Special Global Equity team identifies three current market conditions, including U.S. large cap concentration, high but falling inflation, and attractive small-cap stock valuations, and explores why they may signal a comeback for global small-cap stocks.