Macro Matters: Ahead: More Interest Rate Divergence

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Download PDF

Key takeaways

- While U.S. growth is stabilizing, European economies continue to slow. In China, growth has been underwhelming, but 2025 may bring more stimulus and improving growth data.

- U.S. inflation has been moving toward its 2% target, though future fiscal policy will likely slow progress. Europe’s inflation is below target, and China is experiencing deflation.

- Following December’s U.S. rate cut, we believe future U.S. cuts will likely pause until March. In contrast, cuts in Europe have been more aggressive, and China needs stimulus.

Growth: Can international markets catch up with the U.S.?

The U.S. presidential election’s sentiment boost to markets has benefited U.S. economic growth. In manufacturing, rising new orders and better durable goods orders, plus improved purchasing managers’ reports, point to gradual stabilization and possible reacceleration of growth this year. Strengthening higher-frequency growth indicators combined with a positive Christmas season could push real growth above 3%. (Real growth reflects the value of all goods and services an economy produced while accounting for price fluctuations.) Additional easing by the Federal Reserve (Fed) and fiscal stimulus should help U.S. consumers, who are already benefiting from robust real income and a stable labor market outlook.

Internationally, the growth picture isn’t as favorable. European central banks don’t have a dual mandate of growth and price stability like the Fed does, so the European central banks focus more on stubborn inflation rather than weakening growth. European economies don’t benefit from more aggressive rate cuts yet. Core Europe as well as the U.K. have been slowing lately and might face negative growth for the fourth quarter of 2024. Shorter-term consumer sentiment remains depressed and longer-term challenges like low productivity persist. China’s growth policy has stepped up lately, so 2025 may bring more stimulus. However, potential U.S. trade tariffs pose growth challenges for the eurozone and China.

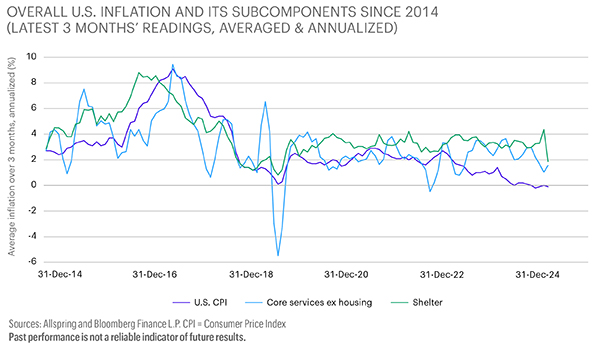

Inflation: Could we see 2% in the U.S. in 2025?

The latest U.S. inflation readings showed slower progress toward the Fed’s target. The preferred consumer-based price measure currently is 2.3% year over year while core inflation (which doesn’t include food and energy costs) is 2.8% for that period. However, real yields remain reasonably tight and should ultimately bring inflation down. The Fed will remain data-dependent and ease just enough to stabilize growth while keeping real rates historically high enough for inflation to drift down. The interest rate market currently expects the Fed to cut rates to somewhere between 3.75% and 4.00% over the course of the year. A lot will depend on how aggressive U.S. fiscal policy turns out to be.

Internationally, some seasonally driven higher inflation readings lately in Europe and the U.K. indicate lower inflation ahead, driven by weak growth and cautious consumers. Eurozone inflation will likely dip substantially below 2% in 2025. China’s inflation outlook remains negative for now.

Rates: A more aggressive pace internationally versus the U.S

Looking at U.S. real yields, one might think there haven’t been any rate cuts yet given that since the first cut in September 2024, nominal and real yields have risen. The good news is that inflation expectations have remained anchored. This points to the Fed’s success at supporting a slowing economy without causing higher prices. It also indicates the Fed has flexibility for cuts in 2025. Fiscal policy will likely remain loose, while trade tariffs could indirectly hit U.S. consumers through higher import prices. The Fed has many factors to consider this year, but its starting position is good: healthy real yields, attractive cash yields, and robust productivity numbers.

Outside the U.S., the situation is trickier. European real yields and productivity are lower, and real growth is weaker. The inflation-versus-growth trade-off is much harder to maneuver for European central banks. Interest rate policy will ultimately need to be more accommodative as growth will likely weaken further. China has already stepped up policy efforts, and more are in the 2025 pipeline. Further rate cuts, lower minimum reserve requirements for banks, and outright fiscal support for consumers are likely to be the main approaches taken.

Implications for fixed income

Conditions for fixed income generally remain very favorable. Spreads are at historical lows, but all-in yields remain attractive. With U.S. growth looking robust, we believe higher-yielding bonds should remain supported and earn the carry. In our view, interest rates will likely continue falling on the short end of the curve and rate cuts will support the long end. Over the short term, we expect volatility to remain elevated. Since rate cuts are already priced in, stronger-than-expected U.S. growth data could lead to some profit-taking in the bond market. Nevertheless, the longer-term picture remains positive. We continue to favor higher-quality U.S. bonds with low- to medium-term durations that we believe should benefit from further rate cuts.

International bonds remain supported by lower growth and inflation. More aggressive rate actions by European central banks have kept their bonds attractive, and emerging market bonds could benefit from more attractive real yields and stabilizing currencies in 2025.

Implications for equities

Entering 2025, we remain constructive on equities. Earnings in the U.S. have been robust, and expectations for 2025 have increased. While technology company earnings have slowed, we believe they’ll remain about double the growth rate of the overall U.S. equity market. That said, volatility will likely increase due to uncertainty around rate cuts, and we may see more rotation into cheaper parts of the U.S. and international equity markets. However, absolute performance will likely be supported by the prospects of gradual monetary easing and fiscal stimulus through corporate tax cuts.

We expect the equity rally to broaden beyond U.S. mega caps into U.S. small caps and international equities, including emerging markets. The latest monetary and fiscal stimuli announced by China’s authorities will likely be ramped up further. Cheaper valuations, lower real rates, and weaker currencies support potential outperformance by emerging market equities. We think focusing on quality and valuation remains a prudent approach.

Implications for multi-asset portfolios

We continue favoring bonds and equities over inflation-sensitive assets. Equities generally rallied following the U.S. elections while bonds struggled after the election outcome as yields rose. Also, we prefer U.S. equities over international equities. Within bonds, we favor shorter over longer maturities because we expect the yield curve to steepen. We also prefer European bonds over U.S. Treasuries given the weaker growth and inflation in the U.K. and eurozone. We changed our U.S. dollar view to positive after the U.S. elections. Despite more expected U.S. rate cuts, the interest rate differential relative to other developed nations is likely to increase and U.S. economic growth is likely to remain stronger, favoring a stronger U.S. dollar.

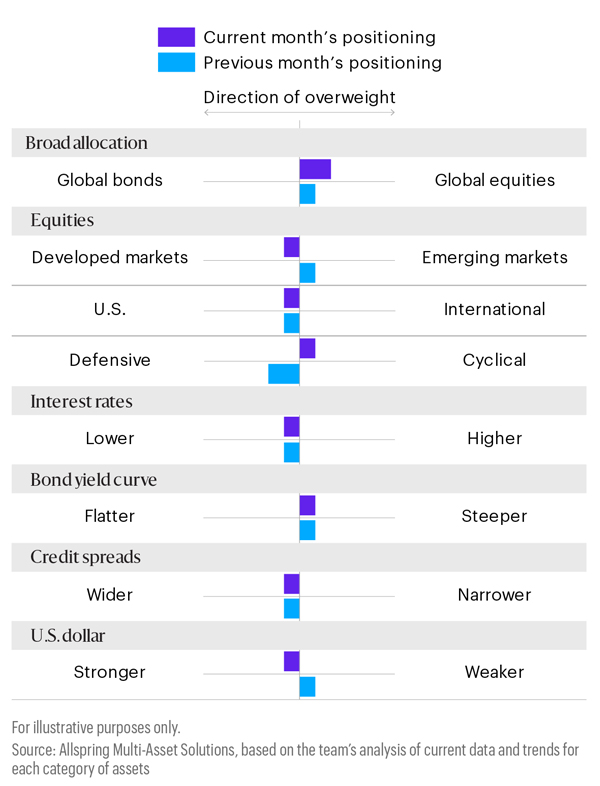

Potential allocations based on today’s environment

The table below depicts our views on short-term trends. These perspectives are developed using quantitative analysis of data over the past 30 years overlaid with qualitative analysis by Allspring investment professionals. The positioning of each bar in the table shows the direction and magnitude of an overweight.

Related insights

Article

A Fine BalanceThe Federal Open Market Committee (FOMC) dropped its key interest rate by 0.25% to 3.50–3.75%. Going into 2026, we see signs that fiscal stimulus will be more meaningful in addressing the current weakening labor market.

Allspring PMs keep their fingers on the pulse of the markets—and their selfie cameras—going into 2026.

George Bory and Ann Miletti share Allspring's 2026 outlook. From resilient bond strategies to AI-powered equity growth, they unpack the key drivers set to shape next year's financial markets.

Which macroeconomic trends do we think matter the most? Read this month’s issue of Macro Matters.

Article

Nothing to See HereDespite limited access to reliable data due to the ongoing government shutdown, the Federal Open Market Committee (FOMC) announced another 0.25% cut, lowering its key interest rate to 3.75–4.00%.

How are Allspring’s investment experts thinking about the U.S. government shutdown and market implications?

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

The Federal Reserve lowered its key rate by 25 basis points at its September meeting following an eight-month pause. George Bory and John Campbell discuss how U.S. bond and equity markets could respond.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

With a robust U.S. economy, above-target inflation, and continued tariff uncertainty, the FOMC kept its key interest rate at 4.25–4.50%.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Speculation over the next chair of the Federal Reserve (Fed) is dominating headlines and keeping markets on edge. A more dovish leader could mean a big shift in monetary policy and raise concerns about the Fed’s independence.

As the events concerning Iran continue, Allspring Fixed Income’s message—"bonds provide certainty in an uncertain world”—remains central to our positioning.

A potential conflict with Iran has consistently appeared in our monthly Market Risk Monitor for over two years. Now that risk has materialized. Our equity portfolio managers assess the implications for global markets.

What might the future hold for markets? In this roundtable discussion, our investment experts explore pressing topics like deficit spending, trade tensions, the Fed’s next moves, and the weakening U.S. dollar.

With ongoing tariff uncertainty and U.S. employment still strong, the Fed kept its key interest rate at 4.25–4.50%.

Amid uncertainty around tariffs and their impact on U.S. growth and inflation, the Federal Reserve held its key interest rate at 4.25–4.50%. We explain what may lie ahead.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

George Bory discusses three key U.S. headlines from April 22 and how fixed income assets may be affected.

George Bory discusses reasons for the recent sharp price fluctuations in stock & bond markets, including in U.S. Treasuries, and identifies actionable approaches fixed income investors may pursue in today’s environment.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Article

Tariffs: A New NormalPresident Trump announced specific details on the administration’s intended trade policy, including a baseline tariff as well as reciprocal tariffs on specific countries. Uncertainty lies ahead as global markets digest the prospects.

At its March meeting today, the Fed kept the federal funds rate at 4.25–4.50% amid concerns around tariffs and their potential impact on U.S. growth and inflation.