Macro Matters: Now Jobs Matter More Than Inflation

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Download PDF

Key takeaways

- We expect gradual slowing in U.S. economic growth ahead but not a stop—internationally, it’s weaker already.

- Inflation’s momentum is pointing in the right direction globally: downward.

- The recent volatility in markets has done some easing work for central banks.

Growth: More weakness ahead

In his latest comments to the U.S. House and Senate, Federal Reserve (Fed) Chair Powell referenced the key areas of focus beyond the inflation rate: The labor market has begun weakening, as supported by the latest employment report, and consumer spending and savings are down. Growth expectations, however, remain robust and supported by expansionary Institute for Supply Management® Services Purchasing Managers’ Index readings. We expect gradual slowing in U.S. economic growth ahead but not a stop.

Internationally, growth data remain mixed with some mild signs of stabilization. Consumer confidence remains weak and savings rates high despite a robust labor market. European business confidence has been negatively affected by the latest elections. The U.K.’s new government has made economic growth a focus, but in the eurozone, governments are restricted by tight budget rules. China remains in a weak position as exports are the only way it can generate growth for now.

Inflation: Downward trend amplified by weaker growth

Fed Chair Powell said he felt May’s Consumer Price Index reading was very good—and this was followed by an even better June print. Service prices (excluding housing and energy) have declined two months in a row, and rents have continued showing lower readings.

Internationally, strong convergence toward inflation targets has continued. The eurozone and the U.K. are basically at target inflation despite some volatility expected in the coming months. That said, the labor market remains reasonably robust. China has seen some small uplift in inflation lately, although at 0.2% year over year, the level indicates deflation if economic growth is truly at an annualized rate of 5.0% as official statistics indicate.

Rates: From divergence to convergence

The recent volatility in markets, which drove strong risk-off sentiment and sent yields materially lower, has done some easing work for central banks. Short-term interest rates in the U.S. are at the extreme in terms of Fed rate cuts, currently pricing in four cuts by the end of 2024. This pricing is not yet backed by the data and economic outlook. As long as the unemployment rate is grinding rather than jumping higher and accompanied by adequate growth, Fed members will likely be data-dependent—they’ll accept some easing but not a full rate-cutting cycle.

Outside the U.S., growth and inflation remain much weaker, so more cuts are justified. International economies also benefit from weaker currencies due to wider interest rate differentials relative to the U.S. given their higher reliance on exports to generate economic wealth. We expect the ECB to cut two more times and the BoE to start cutting rates in the fall.

Implications for fixed income

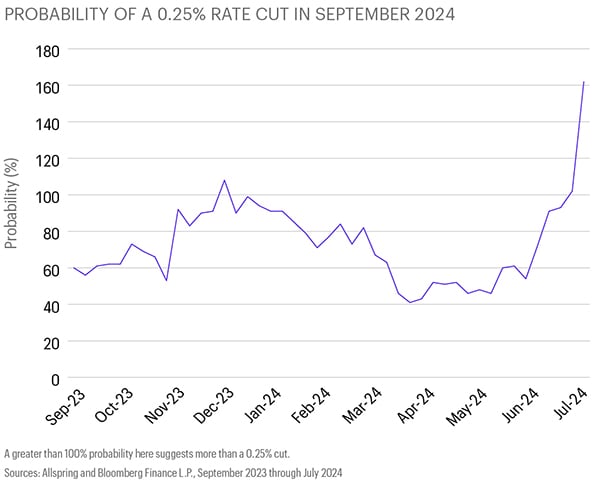

From performance as low as -5.0% at the end of April 2024, the U.S. 10-year bond had recovered nearly all of its losses as of July 23. Increased confidence in a September rate cut has helped U.S. bonds’ total returns while spreads have remained well behaved. As of July 16, U.S. bonds have outperformed German and European government bonds in 2024. We continue to favor bonds with lower durations and higher quality in the U.S. that should benefit from interest rate cuts later this year. International bonds have continued being supported by low growth and inflation, and real yields have continued improving with falling inflation. We believe emerging market bonds should also benefit from a weaker U.S. dollar.

Implications for equities

Similar to fixed income results, U.S. equities have outperformed international equities in 2024 as of July 16. Technology and mega-cap equities have outperformed relative to the broader U.S. market, delivering the edge over international equities.

U.S. value and small-cap equities underperformed as the equity market continued focusing on companies demonstrating strong earnings growth. Equity markets in Europe reacted negatively to France’s snap elections while emerging markets were dragged down by China’s disappointing equity results.

That said, with the increased likelihood of U.S. and international rate cuts, we expect the equity rally to broaden (much like what was seen in the latter half of July) beyond U.S. mega caps into U.S. small caps and international equities, including emerging markets. Cheaper valuations, lower real rates, and weaker currencies all support their potential outperformance. We believe focusing on quality and valuation remains a prudent approach as sector concentration within the U.S. equity market has intensified.

Implications for multi-asset portfolios

A global 60% equity/40% bond portfolio is up more than 8.5% year to date (as of July 16) after strong rallies from the end of April forward in both equities and bonds. Overall, we favor an underweight to commodities and like both equities and bonds.

Within bonds, momentum and valuation remain attractive. As the Fed’s first rate cut potentially approaches in September, we’ve begun favoring shorter-maturity over longer-term bonds as we expect the yield curve to steepen. Within equities, we’ve lowered our preference for large caps over small caps as we expect to see the equity market rally broaden into cheaper areas for the rest of 2024. While the U.S. dollar has remained strong, it’s been range-bound since April. In our view, any further weakening would strengthen the case for exposure to emerging market equities.

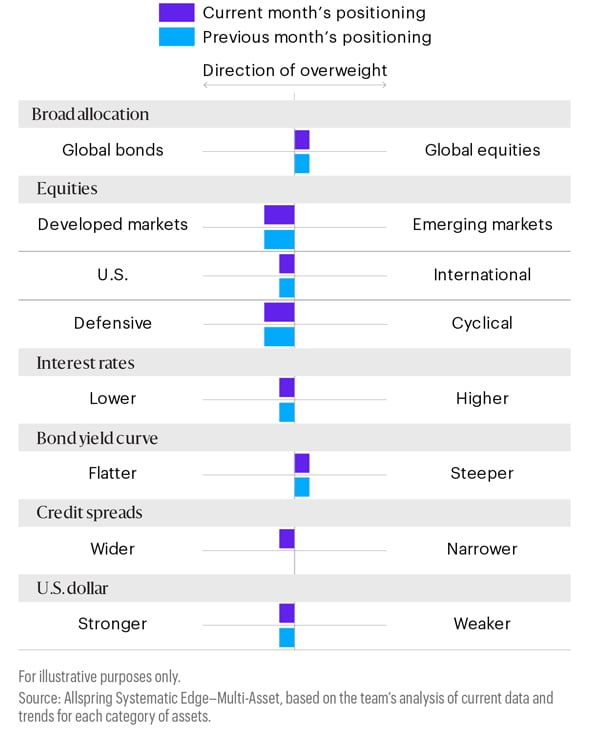

Potential allocations based on today’s environment

The table on the right depicts our views on short-term trends. These perspectives are developed using quantitative analysis of data over the past 30 years overlaid with qualitative analysis by Allspring investment professionals. The positioning of each bar in the table shows the direction and magnitude of an overweight.