Macro Matters—Stagflation: More Damage to Economic Growth?

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

The 3 key takeaways

- Growth: Weakening amid increasing concerns about stagflation

- Inflation: Slower progress toward 2% U.S. target, with uncertain impacts from latest tariffs

- Rates: Federal Reserve (Fed) on hold—internationally, more cuts are needed

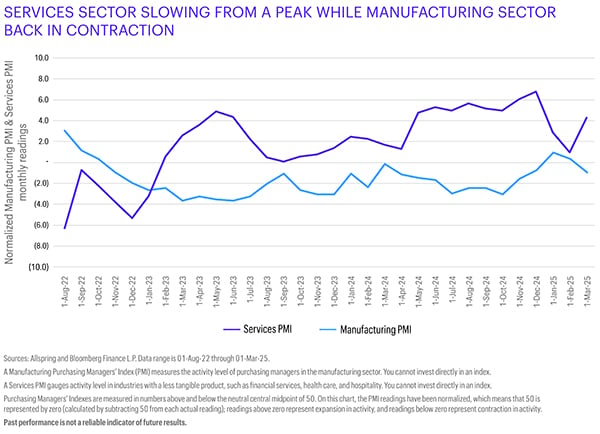

GROWTH: MORE TARIFFS IN APRIL

With the larger-than-anticipated U.S. trade tariffs announced on April 2, growth uncertainty has increased, and we expect that the magnitude by which the global macro environment (growth and inflation) will evolve from here will be volatile. Factors that matter the most include how tariffs are implemented and what reciprocal measures may be implemented by U.S. trading partners.

Our base case is that growth expectations will likely take a hit sooner and inflation expectations will become less anchored over coming weeks and months. U.S. net exports may take years to show a meaningful shift from these tariffs as supply chains and prices reorganize. Prices are unlikely to fall in the short term, despite consumers’ already-weak spending, because businesses generally pass the financial impact of tariffs on to consumers in order to protect margins. The Trump administration’s tariffs announced thus far appear to have exceeded market expectations, triggering strong negative reactions across asset classes. With the volatility, we see potential opportunities revealed for active managers across asset classes when coupled with prudent risk management.

Internationally, growth has stabilized, although the latest European purchasing managers’ data came in weaker than expected, indicating more stimulus is needed to lift consumer sentiment. Germany’s announcement of additional fiscal stimulus has created positive sentiment toward European manufacturing, but it’s unclear how much this will affect domestic consumption. The considerable fiscal stimulus expected in Europe overall might lift employment and domestic consumption if the money finds its way into private-sector innovation and job creation, over the long term. China’s growth continues to benefit from technology innovation, including artificial intelligence developments, and some stabilization in consumer sentiment and the property market.

INFLATION: CONCERNS OVER TARIFFS’ IMPACT ON PRICES

The latest U.S. inflation reading came in a touch lower than expected, with February’s core inflation at 3.1% versus the 3.2% expected. That said, the Fed upgraded its short-term price forecasts and consumers expect higher inflation from more expensive imports. In addition to the latest tariffs, several other measures the Trump administration is taking, such as curbing immigration and focusing on domestic production, will likely drive structurally higher prices, and domestic wages should increase. Commodity prices have been increasing in 2025 due to tariff worries and sharp increases for metals, including copper and gold. Climbing commodity prices could make it more difficult for central banks to manage inflation. Sticky inflation combined with slowing growth data has ignited fears of stagflation.

Outside the U.S., Germany surprised with a lower-than-expected February inflation reading, which might give the European Central Bank (ECB) more room to cut rates this year. In China, inflation dipped into negative territory again. Despite seasonal reasons for the negative reading, the country’s overall consumer prices trend remains deflationary.

RATES: FED ON HOLD, WITH GROWTH VERSUS INFLATION TRADE-OFF WORSENING

As expected, the Fed left rates unchanged in March, and as long as we don’t see signs of a U.S. recession, the Fed will likely stay on hold while assessing incoming data carefully. With the increased trade and growth uncertainties, U.S. growth could easily drop by half—to 1.2% year over year compared with 2024—and the Fed may cut rates more meaningfully in the second half of 2025. As a result, the short-term interest rate market has moved closer to three rate cuts by year-end, up from two cuts at the start of 2025.

U.S. Treasury bonds and international bonds have both been supported by hopes of more rate cuts this year. While fiscal stimulus in the eurozone and the U.S. could make interest rate decisions more difficult over the short term, we expect the ECB and the Bank of England (BoE) to continue rate cuts this year, eventually joined by the Fed later in the year. Although the market expects two more cuts from the ECB and BoE in 2025, we wouldn’t rule out a more aggressive approach if growth data remain lackluster.

IMPLICATIONS FOR FIXED INCOME

With increasing global trade uncertainty and central banks still cautious about adding more stimulus before inflation targets are hit, we believe bond markets should continue doing well. Yields remain attractive overall.

We believe U.S. bonds will remain supported and earn the carry. Interest rates will likely continue falling on the short end of the curve, though probably not before the third quarter of 2025. Farther out on the curve, there’s likely more interest rate volatility ahead because tariffs can potentially increase inflation through higher import prices and a weaker U.S. dollar. We expect the interest rate curve to continue steepening in the second half of 2025 as the market starts rebuilding a term premium into long-maturity bonds. We favor higher-quality U.S. bonds with low- to medium-term durations that are less affected by interest rate and growth volatility.

International bonds remain supported by lower growth and inflation, although this is largely priced in already. We’ll need to see the full effects of the fiscal stimulus through defense spending and how much of it will drive personal consumption higher, rather than the savings rate. We remain positive on international bonds for now.

IMPLICATIONS FOR EQUITIES

We’ve become more cautious on equities in the short term and continue to expect a shift away from the highly concentrated areas of U.S. equities toward more diversified areas, including international equities. A weaker U.S. dollar and lower rates internationally combined with the expected negative impact of U.S. trade tariffs on U.S. consumers have led to international equities’ outperformance. Potentially lower geopolitical risk could boost international stock markets and more fiscal spending could boost U.S. equities, but one of the main drivers remains the fundamental outlook on inflation and how the Fed decides to react going forward.

We expect the global equity market’s broadening to continue—including emerging markets supported by cheaper valuations, lower real rates, weaker currencies, and more Chinese stimulus. Focusing on quality and valuation remains a prudent approach for us.

IMPLICATIONS FOR MULTI-ASSET PORTFOLIOS

Since the beginning of 2025, we’ve been adding to our international equity exposure while reducing U.S. equity exposure. European, emerging market, and Chinese equities could offer good diversification as the rally broadens. We continue to like bonds over cash, especially on the international side. With growth concerns outweighing inflation concerns, we expect to see the equity/bond correlation turn negative again, enabling bonds to become an effective risk diversifier relative to equities. Tariff concerns will likely keep introducing short-term volatility—we’ll need to see how this ultimately affects economic growth. Currently, we favor shorter maturities because we expect a steepening yield curve in Europe. We remain underweight the U.S. dollar given the increased likelihood of trade tariffs triggering negative side effects on growth and inflation.

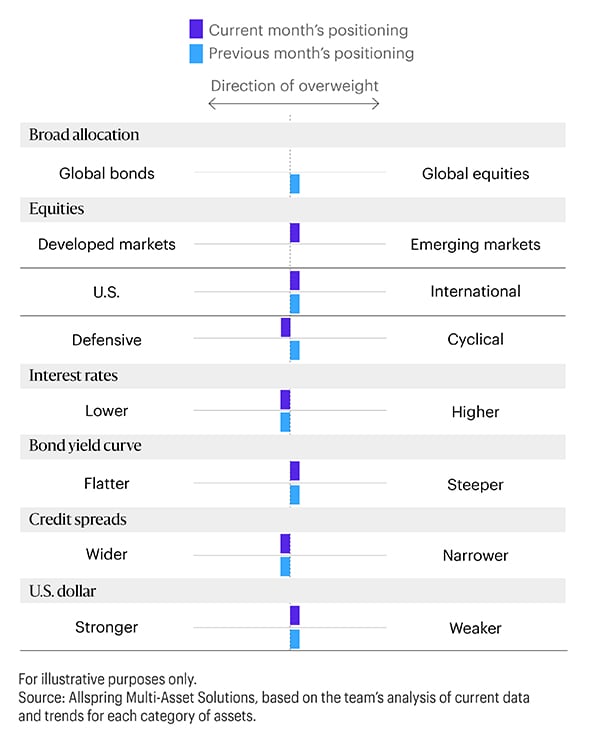

POTENTIAL ALLOCATIONS BASED ON TODAY’S ENVIRONMENT

The table below depicts our views on short-term trends. These perspectives are developed using quantitative analysis of data over the past 30 years overlaid with qualitative analysis by Allspring investment professionals. The positioning of each bar in the table shows the direction and magnitude of an overweight.

ALL-04042025-yng2nk8a

Related insights

George Bory discusses three key U.S. headlines from April 22 and how fixed income assets may be affected.

George Bory discusses reasons for the recent sharp price fluctuations in stock & bond markets, including in U.S. Treasuries, and identifies actionable approaches fixed income investors may pursue in today’s environment.

Article

Tariffs: A New NormalPresident Trump announced specific details on the administration’s intended trade policy, including a baseline tariff as well as reciprocal tariffs on specific countries. Uncertainty lies ahead as global markets digest the prospects.

At its March meeting today, the Fed kept the federal funds rate at 4.25–4.50% amid concerns around tariffs and their potential impact on U.S. growth and inflation.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

The U.S. announced tariffs on Canada, Mexico, and China. Although tariffs on NAFTA countries are temporarily on hold, China is responding with its own retaliatory measures. Allspring experts discuss how these ongoing developments create uncertainty but also opportunities for active portfolio management.

At its January meeting today, the Fed kept the federal funds rate steady at 4.25–4.50%. As the new administration begins implementing its fiscal policy plans, we expect the Fed will remain cautious in monitoring inflation.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Today, as expected, the FOMC announced a cut of 25 basis points in the federal funds rate, lowering it to 4.25%–4.50%. From here, the interest rate path is less clear.

In our 2025 Outlook, we discuss three macro themes we expect in 2025 and nine of our portfolio managers reveal top opportunities they anticipate and their positioning to potentially benefit.

Allspring's investment experts discuss what they believe is ahead for the markets in 2025 and beyond.

Article

Election ReflectionsWith postelection macro trends and the Republican agenda now in the forefront, Allspring’s fixed income teams highlight opportunities and risks for investors to consider in positioning portfolios.

Article

Fed Cuts: One Slice at a TimeAs expected, the FOMC today announced a cut of 25 basis points in the federal funds rate, lowering the rate to 4.50%–4.75%. U.S. election results suggest we could see looser fiscal policy and new trade tariffs ahead, which might lift growth as well as inflation.

Article

Election 2024: Market ImpactsAfter this week’s momentous U.S. election results, Allspring’s investment experts share their perspectives on what to expect for fixed income and equity markets going forward.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Two Allspring equity portfolio managers, Bryant VanCronkhite and Michael Smith, share their perspectives on the U.S. DOJ’s court filing stating it may recommend dismantling Google’s core businesses.

Listen in to George Bory, chief fixed income strategist for Allspring Global Investments, and his immediate reaction on the Wednesday, September 18, announcement from the FOMC (Federal Open Market Committee) meeting.

The Fed decided to finally lower its key interest rate, announcing a cut of 50 basis points, to 4.75–5.00%. A cut of at least 25 basis points was widely expected and welcomed.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Macro Matters provides a concise, comprehensive look at macroeconomic themes that matter to clients.

Fed officials again kept the federal funds rate at 5.25–5.50%. We believe they’ll cut for the first time this cycle in September and then analyze incoming data to inform future rate-cut decisions.

When uncertainty is high, it’s important for bond investors to prioritize flexibility. Making small decisions across multiple sectors while maintaining investment flexibility is preferable to one big macro view.