Investing

Climate Transition Opportunity In Fixed Income

Seeking dual climate and financial outcomes through a proprietary framework that hit its three-year milestone in January 2024.

As the world transitions towards net-zero emissions, new opportunities and risks are opening up across markets. We believe investors need to consider repositioning their portfolios to best capture these new opportunities and manage unintended risks.

Grounded in a proven and successful investment process, Allspring has responded with a suite of climate transition credit strategies.

Allspring’s Climate Transition Framework**, married with our deep fixed income expertise, enables investors to gain exposure to the climate transition leaders of today and tomorrow, whilst also being centrally focused on meeting their financial goals.

Why fixed income for climate transition?

For clients seeking to help decarbonise the world, we believe fixed income plays a critical role and continues to represent an attractive opportunity. Why should clients focus on fixed income when investing for climate transition? We point to three reasons:

1. Financial return

Allocating capital to companies that are actively positioning themselves for a net-zero world can help avoid stranded assets and potentially increase the probability that investors will receive expected coupon and redemption payments.

2. Carbon intensity

The average weighted carbon intensity of fixed income can be higher than main equity indices.* As such, fixed income assets can be a key tool in the decarbonisation arsenal.

3. Engagement

Bondholders can make a difference through active engagement. This gives investors in credit a real opportunity to drive change. Access to capital and cost of capital are powerful levers for bondholders when engaging.

*S&P Trucost, as at 31-Dec -22

How we invest in climate transition credit

Allspring’s Climate Transition Credit approach is designed to rigorously assess investment opportunities and their associated risks and deliver optimum investor outcomes through a combined climate and financial lens.

Picking climate transition credit leaders

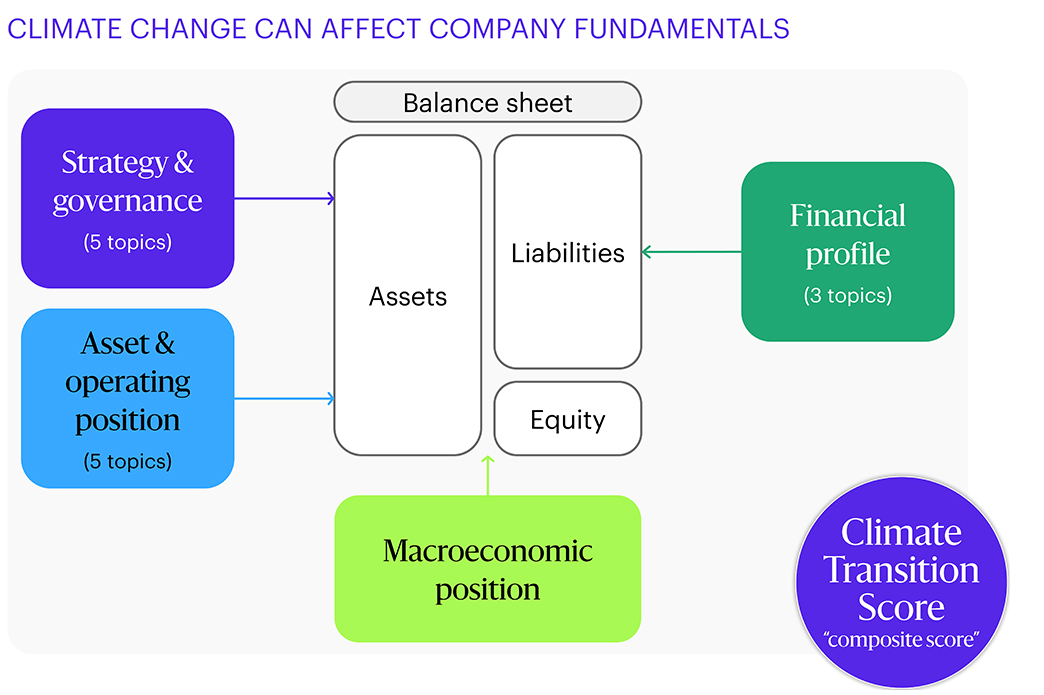

Using our Climate Transition Framework**, our fundamental analysts draw and build upon their deep knowledge to evaluate and score the implications of climate change on company fundamentals.

Using proprietary data and systems, our analysts fully integrate four primary categories of climate risk and opportunity—based on dozens of climate risk metrics—into their holistic, forward-looking view of the company. Companies that stand to make the most meaningful contributions to decarbonisation whilst benefitting fundamentally are prioritised in security selection. Companies that screen poorly become ineligible for portfolios.

** Our fundamental analysts evaluate the implications of climate change on company fundamentals on 14 topics across four pillars, rating each with a climate transition score between 1 and 4, importantly with a trend indicator.

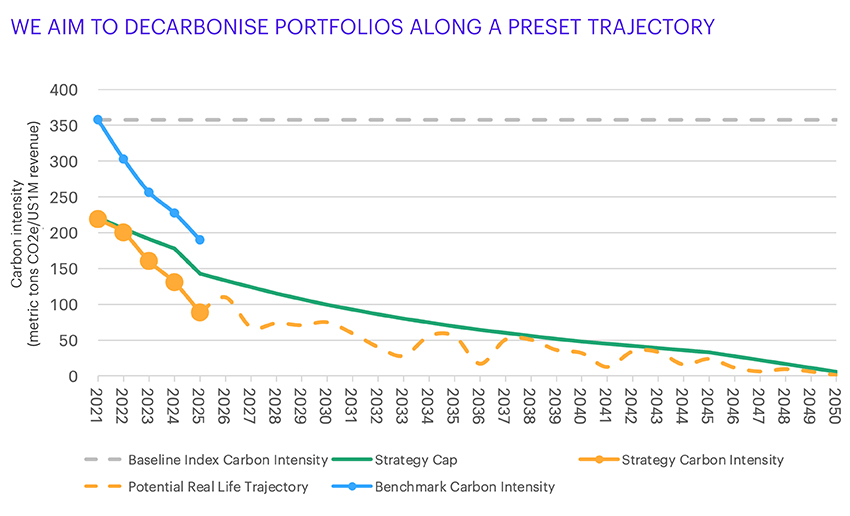

Targeting an ambitious decarbonisation profile

Our strategies align with a transparent, consensus-based trajectory that is part of European Union climate benchmark policies. Key features include targeting an overall carbon intensity for the portfolio that is at least 30% lower than the benchmark and aims to decarbonise by 2050.

For illustrative purpose only. Source: Allspring and Trucost, as at 31 March 2025.

Targeted exclusion to optimize performance

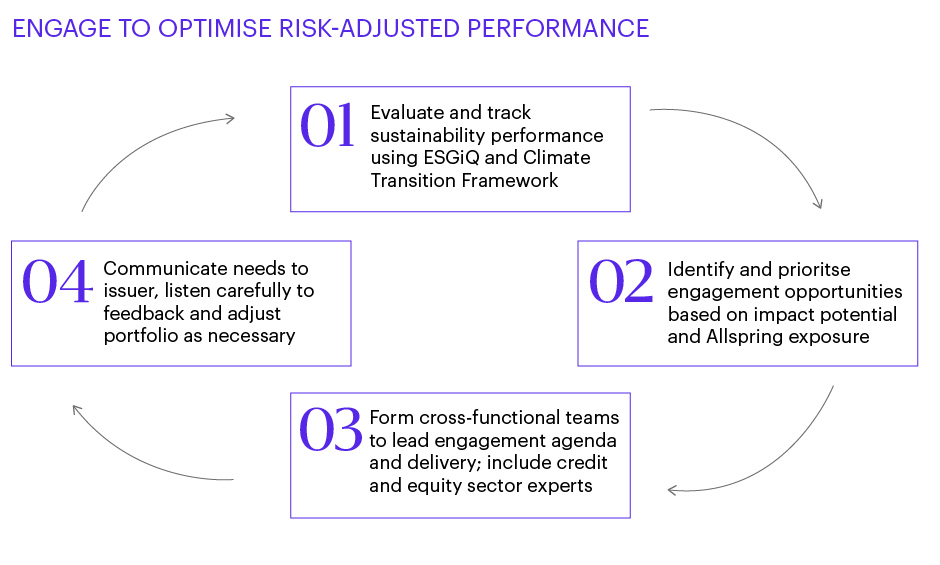

We prioritise corporate engagement by impact potential, including the systemic importance of climate change itself, strategy-level exposure and our overall exposure. We do not automatically exclude industries with high historical carbon emissions; instead, we focus on companies' forward transition performance. Our inclusive approach, partnering with our fundamental equity and credit teams, is a key differentiator of how we engage.

Leveraging Allspring's ESGIQ risk-assessment framework to identify leaders and laggards

ESGIQ is a proprietary rating system we created to assess ESG risk. Our methodology enhances data from third-party providers with our analysts’ in-depth sector knowledge and expertise. The rating frame leverages high-quality ESG data and analyses from leading external data providers, enabling broader coverage than what is available from a single provider. Assessment by our fundamental investment analysts complements the vended data to ensure timeliness as well as capturing trends. We use a simple 1-through-5 scale, with 5 being the best, to articulate our assessment.

Your team of experts

Leveraging our global Fixed Income Platform resources with sustainable investing expertise, our sustainable investing professionals welcome the opportunity to partner with you to explore your objectives and help you pursue your goals.

Featured insights

Insight

Eye on SI: 2026 OutlookWhat are the key trends driving investment opportunities and concerns for sustainability in 2026? Our Sustainability Outlook focuses on three—all of which relate to the surge in artificial intelligence (AI) and energy transition.

The 30th United Nations Conference of the Parties (COP30) is likely to deliver incremental rather than transformative progress, as most countries remain misaligned with the Paris Agreement and net-zero pathways.

Insight

2024 Stewardship Annual ReportRead about Allspring’s stewardship efforts in this year’s annual report. We aim to advance the financial, operational, and sustainability performance and risk management of investee companies for years to come.

Also available—an equity solution. Learn more:

All investments contain risk, including market risk, liquidity risk and exchange rate risk. The value, price or income of investments or financial instruments can fall as well as rise and is not guaranteed. You may not get back the amount originally invested.